Only employed members of the CERN personnel (fellow or staff) and employed members of ESO (fellow or staff), in accordance with the CERN/ESO Agreement.

How do I Join the Fund?

As an employed member of the CERN/ESO personnel (fellow or staff), subject to the conditions specified in the CERN/ESO Agreement, you will automatically join the Fund, as membership is compulsory. Your contribution is automatically deducted from your monthly salary.

How is my contribution to the Fund calculated?

As a CERN/ESO staff member or ESO fellow, contributions are based on your monthly CHF reference salary and calculated using the following rates:

a) If you joined the Fund on or before 31 December 2011:

Member: 11.33%

Organisation: 22.67%

b) If you joined the Fund on or after 1 January 2012:

Member: 12.64%

Organisation: 18.96%

As a CERN fellow, your contributions are based on a fixed reference salary of 6 453 CHF and calculated using the rates above.

As a CERN GRAD, your contributions are based on a fixed reference salary of 5 826 CHF and calculated using the rates above.

Contributions

How can I calculate my reference salary?

As an employed member of the CERN/ESO personnel, the reference salary is: basic salary for 40 hours per week multiplied by the applicable C factor.

If you are a CERN fellow (junior or senior), the reference salary is: 4 844 CHF multiplied by the applicable C factor, which is 1.3322.

If you are a CERN GRAD, the reference salary is: 4 373 CHF multiplied by the applicable C factor, which is 1.3322.

As a CERN/ESO staff member or ESO fellow, contributions are based on your monthly CHF reference salary and calculated using the following rates:

a) If you joined the Fund on or before 31 December 2011:

Member: 11.33%

Organisation: 22.67%

b) If you joined the Fund on or after 1 January 2012:

Member: 12.64%

Organisation: 18.96%

As a CERN fellow, your contributions are based on a fixed reference salary of 6 453 CHF and calculated using the rates above.

As a CERN GRAD, your contributions are based on a fixed reference salary of 5 826 CHF and calculated using the rates above.

Where can I find my CHF reference salary?

As a member of the CERN personnel, your reference salary can be found on your payslip under “CONTRIB. PENSION”.

As a member of the ESO personnel, you can calculate your reference salary using the data provided on your payslip under “Pension CERN” (basic salary in CHF x C factor).

Can I increase or decrease my contributions or stop contributing to the Fund?

The contribution rates are defined in the CERN Pension Fund Rules and Regulations. Only in certain cases (such as unpaid special leave, parental leave, part-time work, etc.) will you have the option to suspend or reduce your contributions.

My Benefits

I am working part time. What is the impact on my benefits?

If you decide to continue to contribute at 100%, there is no impact on your benefits.

If you decide to contribute pro rata, your benefits will be reduced accordingly, due to the reduced level of contributions.

I am leaving on unpaid special/parental leave. What is the impact on my benefits?

If you decide to continue to contribute at 100%, there is no impact on your benefits.

If you decide to contribute pro rata, your benefits will be reduced accordingly, due to the reduced level of contributions.

What is the applicable retirement age?

For members who joined the Fund:

before 1 January 2012, the official retirement age is 65;

on or after 1 January 2012, the official retirement age is 67.

What is the maximum period of membership?

For members who joined the Fund:

before 1 January 2012: 35 years;

on or after 1 January 2012: 37 years and 10 months.

Can I take my pension before the applicable retirement age and, if so, when? What is the impact on my benefits?

You can ask for an early retirement pension:

as from 50 years of age, if you joined the fund before 1 January 2012

as from 52 years of age, if you joined the fund on or after 1 January 2012.

A reduction factor is applied to your benefits :

Amount of early Retirement Pension (Article II 2.05)

Article II 2.05 Amount of Early Retirement Pension

The early retirement pension shall be calculated by multiplying the amount of the deferred retirement pension by the appropriate factor in the following tables:

a) For members who joined the Fund on or before 30 June 1987

Age at first payment of the early retirement pension

Factor (%)

60 to 64

100.0

59

93.3

58

87.2

57

81.7

56

76.7

55

72.1

54

67.8

53

63.9

52

60.3

51

57.0

50

54.0

b) For members who joined the Fund between 1 July 1987 and 31 December 2011, inclusive

Age at first payment of the early retirement pension

Factor (%)

64

94.7

63

89.9

62

85.4

61

81.2

60

77.3

59

73.7

58

70.4

57

67.2

56

64.3

55

61.5

54

58.9

53

56.4

52

54.1

51

51.9

50

49.9

c) For members who joined the Fund on or after 1 January 2012

Age at first payment of the early retirement pension

Factor (%)

66

94.5

65

89.4

64

84.7

63

80.4

62

76.4

61

72.7

60

69.2

59

66.0

58

63.0

57

60.2

56

57.6

55

55.1

54

52.8

53

50.6

52

48.5

For the purposes of application of Article II 2.05 of the Rules of the Fund, periods falling between two factors are calculated in months in accordance with the linear interpolation method.

Do I have to pay taxes on my transfer value?

Pensions and other benefits, such as transfer value, are taxable under conditions defined in the national fiscal legislation which is applicable to the person concerned.

I am affiliated to the CERN life insurance. Can I remain a member when I leave?

Yes, if you become a beneficiary of a retirement or disability pension and as long as you have been affiliated for at least five years before your contract end date.

I would like to increase my benefits. How can I do this?

Transfer from another pension scheme: the CERN Pension Fund accepts transfers from worldwide pension schemes. Please contact your previous pension scheme to make sure that the transfer can be made.

Own fund purchase: you have the option to buy periods of membership with your own funds. This kind of purchase is calculated according to a rate and based on your reference salary at the time of the request, your age at the time of the request and your age when your membership began. The purchase can be paid for in either a lump sum or instalments (payment in instalments will be subject to interest and must not exceed three years).

My Family Benefits

Do my spouse and children have rights in the event of my death?

Your spouse has the right to a surviving spouse’s pension if your marriage lasts for at least a year (unless you have dependent children, in which case this condition does not apply).

Your children have the right to an orphan’s pension for as long as they are considered as dependent.

In the event of divorce, does my ex-spouse still have rights in the event of my death?

Your ex-spouse has rights after your death only if you were paying maintenance, if she/he is at least 45 years of age and if the marriage lasted for at least 10 years.

Purchase/Transfer from other scheme

Before coming to CERN, I contributed to other pension schemes. Can I transfer other pension assets into the CERN Pension Fund?

Yes, the CERN Pension Fund accepts transfers from pension schemes in which provision is made for contributions by the employer. Please first contact your previous scheme to ensure that a transfer to the CERN Pension Fund is permitted (as some schemes do not allow this).

I would like to fill gaps in my pension during my career. How can I do this?

Transfer from another pension scheme: the CERN Pension Fund accepts transfers from pension schemes in which provision is made for contributions by the employer. Please contact your previous pension scheme to ensure that a transfer is permitted.

Purchase using own funds: if you have already accrued five years of service, you have the option to buy added periods of membership with your own funds. This type of purchase is calculated according to rates defined in chapter III of the Fund’s Regulations and your reference salary at the time of the request.

As a member of the CERN personnel, your reference salary can be found on your payslip under “CONTRIB. PENSION”.

As a member of the ESO personnel, you can calculate your reference salary using the data provided on your payslip under “Pension CERN” (basic salary in CHF x C factor).

How can I calculate my reference salary?

As an employed member of the CERN/ESO personnel, the reference salary is: basic salary for 40 hours per week multiplied by the applicable C factor.

If you are a CERN fellow (junior or senior), the reference salary is: 4722 CHF multiplied by the applicable C factor, which is 1.3322.

If you are a CERN GRAD, the reference salary is: 4263 CHF multiplied by the applicable C factor, which is 1.3322.

Beneficiaries

Future/New Beneficiaries

When do I receive my statement of declaration of income?

In February each year, you will receive a “Statement of declaration of your income”.

My Benefits

I am entitled to a deferred retirement pension and would like to receive it as an early retirement pension, what should I do?

Please contact the Benefits Service at least three months before the chosen early retirement date.

Where can I find the Swiss franc/Euro exchange rate used in my declaration of income?

The exchange rate is published by the tax office in April and communicated in the CERN Bulletin.

I would like to fill gaps in my pension during my career. How can I do this?

Transfer from another pension scheme: the CERN Pension Fund accepts transfers from pension schemes in which provision is made for contributions by the employer. Please contact your previous pension scheme to ensure that a transfer is permitted.

Purchase using own funds: if you have already accrued five years of service, you have the option to buy added periods of membership with your own funds. This type of purchase is calculated according to rates defined in chapter III of the Fund’s Regulations and your reference salary at the time of the request.

Annual adjustment

How do I know which method in Annex C of the Rules applies to my situation?

The applicable method depends on your personal situation and particular dates. To determine which method is relevant, please refer to the following guidance:

If you are a beneficiary of a retirement or total disability pension, the date that you became a beneficiary corresponds to your pension start date.

If you are a beneficiary of a surviving spouse’s pension or an orphan’s pension, the relevant date is the date when the deceased beneficiary became a beneficiary.

If you are a beneficiary of a retirement pension having participated in the Progressive Retirement Program (PRP), the date you became a beneficiary corresponds to your PRP start date.

If you are a beneficiary of a surviving spouse’s pension or an orphan’s pension following the death of a member, the relevant date is your pension start date.

Should your date be:

on or before 31 December 2011, the applicable method would be I. 1. of Annex C.

between 1 January 2012 and 31 July 2019, the applicable method would be I. 2. of Annex C.

on or after 1 August 2019, the applicable method would be I. 3. of Annex C.

Annex C – Method for the Annual Adjustment of Pension (Article II 1.14)

Definitions

PPL: purchasing power loss.

PPL Account: individual accumulated loss of purchasing power account maintained for each beneficiary, the balance of which shall not exceed 8%.

Geneva CVI: annual variation of the Geneva consumer price index for the last twelve-month period (August to August), expressed in percentage points.

Funding ratio: actual funding ratio of the Fund in a closed fund technical balance sheet as confirmed in the annual financial statements of the Fund approved by the Council.

I. Method for the Annual Adjustment of Pensions

The method applicable for the annual adjustment of pensions differs pursuant to the date on which a person becomes a beneficiary of a pension.

1. Method for the annual adjustment of pensions for persons who became beneficiary of a pension on or before 31 December 2011

a) Persons who became beneficiary of a pension on or before 31 December 2011 shall receive no annual adjustment of pension unless their PPL account maintains a balance of 8%. Provided their PPL account has such a balance, the method set out in paragraphs 1 (b) and (c) shall apply.

b) (i) If the Geneva CVI is positive, the annual adjustment shall be the Geneva CVI, unless the conditions of 1 (c) are fulfilled;

(ii) If the Geneva CVI is zero, no annual adjustment shall be granted;

(iii) If the Geneva CVI is negative, no annual adjustment shall be granted but the resulting effective increase in purchasing power shall reduce the balance of the beneficiary’s PPL account.

c) When the funding ratio of the Fund has been greater than 110% for three consecutive years, beneficiaries who have incurred an individual accumulated loss of purchasing power shall be compensated as follows: provided that the Geneva CVI is positive and the funding ratio remains greater than 110%, their annual adjustment of pensions shall be the product of the Geneva CVI multiplied by the funding ratio, until such time as the balance of their PPL account is reduced to zero.

2. Method for the annual adjustment of pensions for persons who become beneficiary of a pension between 1 January 2012 and 31 July 2019

a) Persons who become beneficiary of a pension between 1 January 2012 and 31 July 2019, inclusive, shall receive no annual adjustment of pension unless their PPL account maintains no less than the minimum balance set out in Table 1. Provided their PPL account has such a balance, the method set out in paragraphs 2 (b) and (c) shall apply.

b) (i) If the Geneva CVI is positive and the funding ratio is less than 100%, the adjustment shall be the product of the Geneva CVI multiplied by the funding ratio, up to a maximum of the actuarial parameter for annual inflation as set out in the Actuary’s triennial report, always provided that no PPL account may exceed a balance of 8%1 ;

(ii) If the Geneva CVI is positive and the funding ratio is equal to or greater than 100%, the annual adjustment shall be the Geneva CVI, unless the conditions of 2 (c) are fulfilled;

(iii) If the Geneva CVI is zero, no annual adjustment shall be granted;

(iv) If the Geneva CVI is negative, no annual adjustment shall be granted but the resulting effective increase in purchasing power shall reduce the balance of the beneficiary’s PPL account.

c) When the funding ratio of the Fund has been greater than 110% for three consecutive years, beneficiaries who have incurred an individual accumulated loss of purchasing power shall be compensated as follows: provided that the Geneva CVI is positive and the funding ratio remains greater than 110%, their annual adjustment of pensions shall be the product of the Geneva CVI multiplied by the funding ratio, until such time as the balance of their PPL account is reduced to zero.

3. Method for the annual adjustment of pensions for persons who become beneficiary of a pension on or after 1 August 2019

a) Persons who become beneficiary of a pension on or after 1 August 2019 shall be granted an annual adjustment in accordance with the method set out in paragraphs 3 (b) and (c).

b) (i) If the Geneva CVI is positive and the funding ratio is less than 100%, the adjustment shall be the product of the Geneva CVI multiplied by the funding ratio, up to a maximum of the actuarial parameter for annual inflation as set out in the Actuary’s triennial report, always provided that no PPL account may exceed a balance of 8%2 ;

(ii) If the Geneva CVI is positive and the funding ratio is equal to or greater than 100%, the annual adjustment shall be the Geneva CVI, unless the conditions of 3 (c) are fulfilled;

(iii) If the Geneva CVI is zero, no annual adjustment shall be granted;

(iv) If the Geneva CVI is negative, no adjustment shall be granted but the resulting effective increase in purchasing power shall reduce the balance of the beneficiary’s PPL account.

c) When the funding ratio of the Fund has been greater than 110% for three consecutive years, beneficiaries who have incurred an individual accumulated loss of purchasing power shall be compensated as follows: provided that the Geneva CVI is positive and the funding ratio remains greater than 110%, their annual adjustment of pensions shall be the product of the Geneva CVI multiplied by the funding ratio, until such time as the balance of their PPL account is reduced to zero.

II. Method for the Annual Adjustment of the Fixed Sum and Allowances

The fixed sum and allowances shall be adjusted annually in accordance with the applicable method for the annual adjustment of pensions as set out above.

1 If a beneficiary’s PPL account maintains a balance of 8% and the Geneva CVI is positive, the Geneva CVI shall be granted notwithstanding the funding ratio of the Fund.

2 If a beneficiary’s PPL account maintains a balance of 8% and the Geneva CVI is positive, the Geneva CVI shall be granted notwithstanding the funding ratio of the Fund.

How do I know what my current purchasing power loss (PPL) balance is?

Every year in December you receive a letter from the Fund with information on the annual adjustment to your benefits effective 1 January the following year. The letter includes your updated purchasing power loss (PPL) balance for the coming year.

Which funding ratio is used in the annual adjustment calculation?

The funding ratio used in the annual adjustment calculation is the funding ratio on an accounting basis and is included in the Statement of Financial Position of the Pension Fund’s last audited Financial Statements.

Which Geneva Cost of living (CVI) is used in the annual adjustment calculation?

The Geneva CVI used in the annual adjustment calculation is Geneva CVI for the last twelve-month period from August to August.

My adjustment calculation depends on the actuarial parameter for annual inflation but where can I find this?

The actuarial parameter for annual inflation, from the last periodic actuarial review, is noted in the actuarial section of the Fund’s Annual Report.

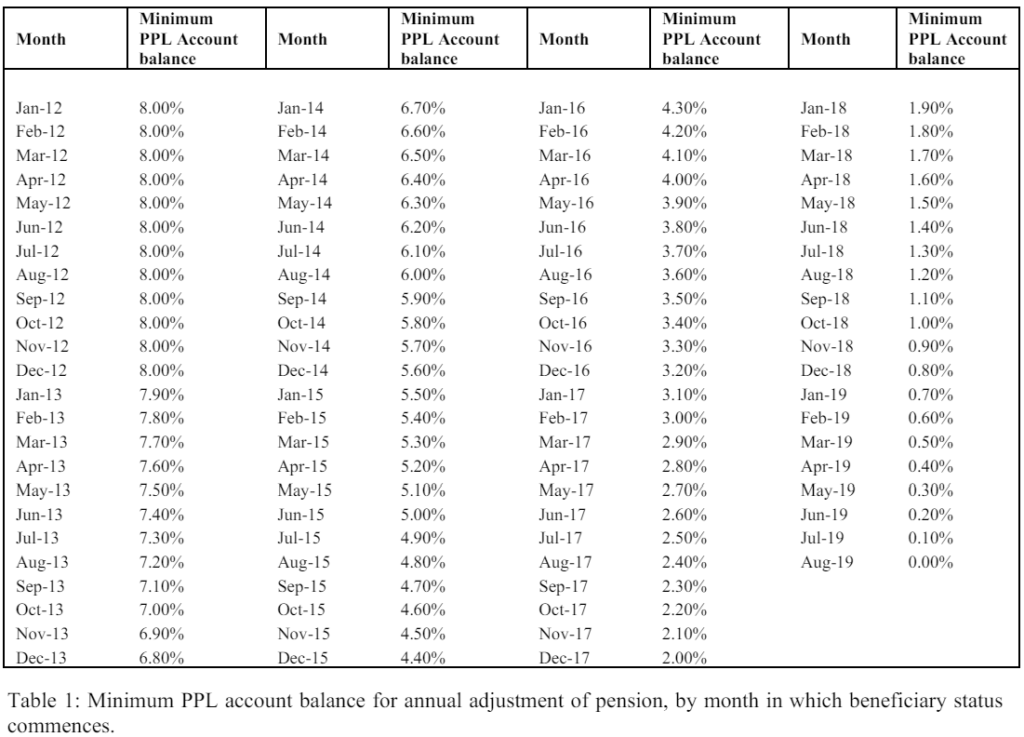

If it is relevant to my situation, what is my minimum PPL account balance?

If, between 1 January 2012 and 31 July 2019:

You became a beneficiary,

You are a surviving spouse or orphan of a deceased beneficiary who became a beneficiary of a pension,

You entered into the Progressive Retirement Program (PRP), or

You are a surviving spouse or orphan of a member who passed away,

You have a minimum PPL account balance. It is based on the month and year of one of the above situations. Your minimum PPL account balance is used to determine whether you will receive an annual adjustment. You will not receive an annual adjustment unless your individual accumulated PPL balance has reached your minimum PPL account balance. The different minimum PPL account balances are set out in Table 1 of Annex C of the Rules and Regulations.

Table 1 – Annex C: Annual adjustment for persons who become beneficiary of a pension between 1 January 2012 and 31 July 2019

a) Persons who become beneficiary of a pension between 1 January 2012 and 31 July 2019, inclusive, shall receive no annual adjustment of pension unless their PPL account maintains no less than the minimum balance set out in Table 1. Provided their PPL account has such a balance, the method set out in paragraphs 2 (b) and (c) shall apply.

b) (i) If the Geneva CVI is positive and the funding ratio is less than 100%, the adjustment shall be the product of the Geneva CVI multiplied by the funding ratio, up to a maximum of the actuarial parameter for annual inflation as set out in the Actuary’s triennial report, always provided that no PPL account may exceed a balance of 8%1 ;

(ii) If the Geneva CVI is positive and the funding ratio is equal to or greater than 100%, the annual adjustment shall be the Geneva CVI, unless the conditions of 2 (c) are fulfilled;

(iii) If the Geneva CVI is zero, no annual adjustment shall be granted;

(iv) If the Geneva CVI is negative, no annual adjustment shall be granted but the resulting effective increase in purchasing power shall reduce the balance of the beneficiary’s PPL account.

c) When the funding ratio of the Fund has been greater than 110% for three consecutive years, beneficiaries who have incurred an individual accumulated loss of purchasing power shall be compensated as follows: provided that the Geneva CVI is positive and the funding ratio remains greater than 110%, their annual adjustment of pensions shall be the product of the Geneva CVI multiplied by the funding ratio, until such time as the balance of their PPL account is reduced to zero.

1 If a beneficiary’s PPL account maintains a balance of 8% and the Geneva CVI is positive, the Geneva CVI shall be granted notwithstanding the funding ratio of the Fund.

Why am I not receiving an annual adjustment?

As a beneficiary you have an individual PPL account. This is the individual account maintained for each beneficiary with the accumulated loss of purchasing power i.e. the difference between Geneva CVI and your annual adjustments. Your individual accumulated PPL balance has not reached 8% or your minimum PPL balance so no adjustment is granted.

What happens if Geneva CVI is zero?

If Geneva CVI is zero then you will not receive an annual adjustment.

What happens if Geneva CVI is negative?

If Geneva CVI is negative then you will not receive an annual adjustment, however your PPL account balance will be reduced accordingly, and your benefits will remain unchanged.

Life Insurance

Can I modify my insured capital and, if so, how?

You can only reduce your capital (30 days notice). Please complete the form and return the original, signed in ink, to the Fund’s Benefits Service.

I would like to change the beneficiaries of my life insurance. How can I do this?

You should complete the form and return the original, signed in ink, to the Fund’s Benefits Service.

I would like to terminate my membership of the life insurance scheme. How can I do this?

Please send, by post only, a signed resignation letter (giving 30 days’ notice) to the Benefits Service.

Pension Payment

Can my pension be paid in a country other than Switzerland?

Yes, provided that operational requirements are met (e.g. standard international IBAN payments must be supported) benefits may be paid in a CERN/ESO Member State or Associate Member State. Payments are made in Swiss francs and any bank or transfer fees would be at your expense.

When is my pension paid?

Pensions are paid monthly, in advance, between 6 and 8 of the month.

Do I receive a monthly statement of my benefits?

No, there is no monthly pay notification; however, every January, beneficiaries receive a monthly breakdown valid for the entire year. If the beneficiary’s personal situation changes, an updated monthly breakdown will be sent.

Where can I find the Swiss franc/Euro exchange rate used in my declaration of income?

The exchange rate is published by the tax office in April and communicated in the CERN Bulletin.