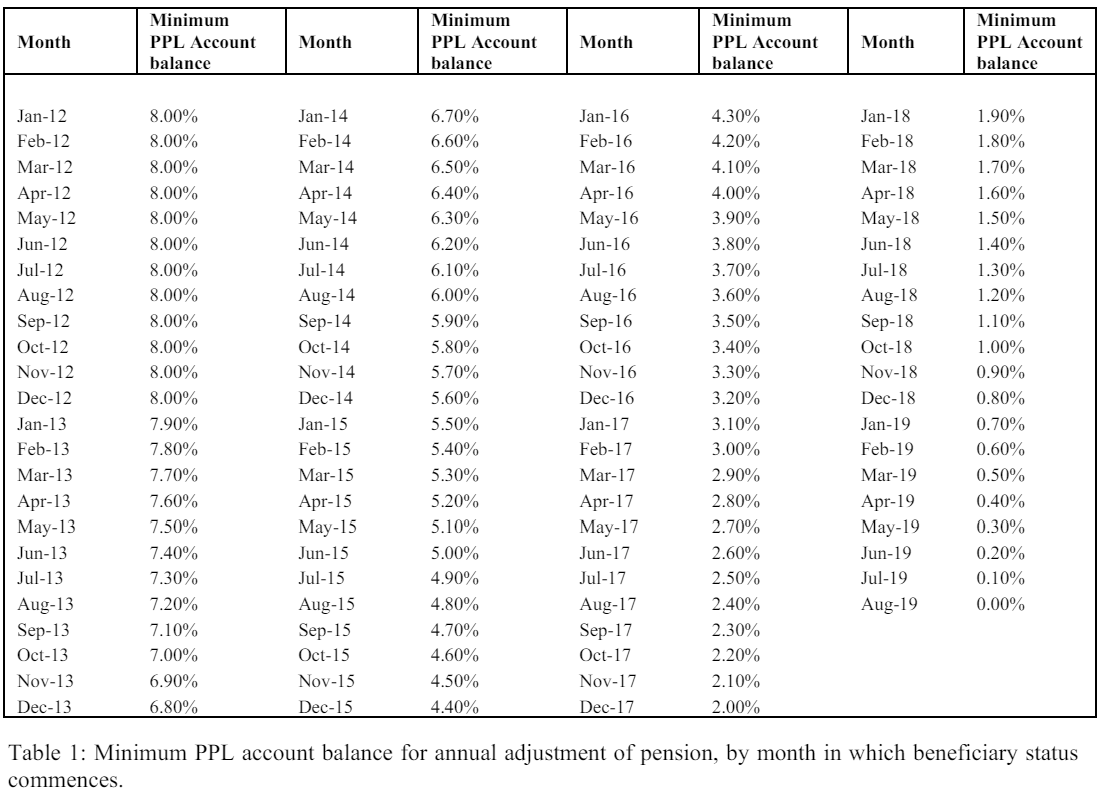

a) Persons who become beneficiary of a pension between 1 January 2012 and 31 July 2019, inclusive, shall receive no annual adjustment of pension unless their PPL account maintains no less than the minimum balance set out in Table 1. Provided their PPL account has such a balance, the method set out in paragraphs 2 (b) and (c) shall apply.

b) (i) If the Geneva CVI is positive and the funding ratio is less than 100%, the adjustment shall be the product of the Geneva CVI multiplied by the funding ratio, up to a maximum of the actuarial parameter for annual inflation as set out in the Actuary’s triennial report, always provided that no PPL account may exceed a balance of 8%1 ;

(ii) If the Geneva CVI is positive and the funding ratio is equal to or greater than 100%, the annual adjustment shall be the Geneva CVI, unless the conditions of 2 (c) are fulfilled;

(iii) If the Geneva CVI is zero, no annual adjustment shall be granted;

(iv) If the Geneva CVI is negative, no annual adjustment shall be granted but the resulting effective increase in purchasing power shall reduce the balance of the beneficiary’s PPL account.

c) When the funding ratio of the Fund has been greater than 110% for three consecutive years, beneficiaries who have incurred an individual accumulated loss of purchasing power shall be compensated as follows: provided that the Geneva CVI is positive and the funding ratio remains greater than 110%, their annual adjustment of pensions shall be the product of the Geneva CVI multiplied by the funding ratio, until such time as the balance of their PPL account is reduced to zero.

1 If a beneficiary’s PPL account maintains a balance of 8% and the Geneva CVI is positive, the Geneva CVI shall be granted notwithstanding the funding ratio of the Fund.